The topic of environment and sustainability is on everyone’s lips, yet the confusion is immense. An attempt to summarize the issues in one sentence could be something like this: Environmental protection focuses on the protection and preservation of our natural resources, while sustainability also incorporates economic and social aspects.

Our Goals!

Our Goals!

CSRD, ESRS, ESG, SDG, CSDDD, DNK – there’s a bewildering array of terms relating to European regulations, federal laws, reporting requirements, and certifications. The topic of sustainability is increasingly becoming a focus of corporate activity. However, the foundation is always knowledge of the determined environmental indicators, which must always be recorded first. Only with carefully determined environmental indicators can the step toward sustainability reporting be taken.

Our Services!

We offer support for the (initial) determination of environmental indicators based on a life cycle assessment or – if you have already determined these – for their verification. Based on the environmental indicators, we create a carbon footprint. This serves as the basis for the sustainability report, which can be prepared on various bases. The German Sustainability Code (DNK) is the most popular version; it is part of the “Rat für Nachhaltige Entwicklung” (German Council for Sustainable Development), which advises the German Federal Government. As a third step, the company can participate in an external assessment or rating.

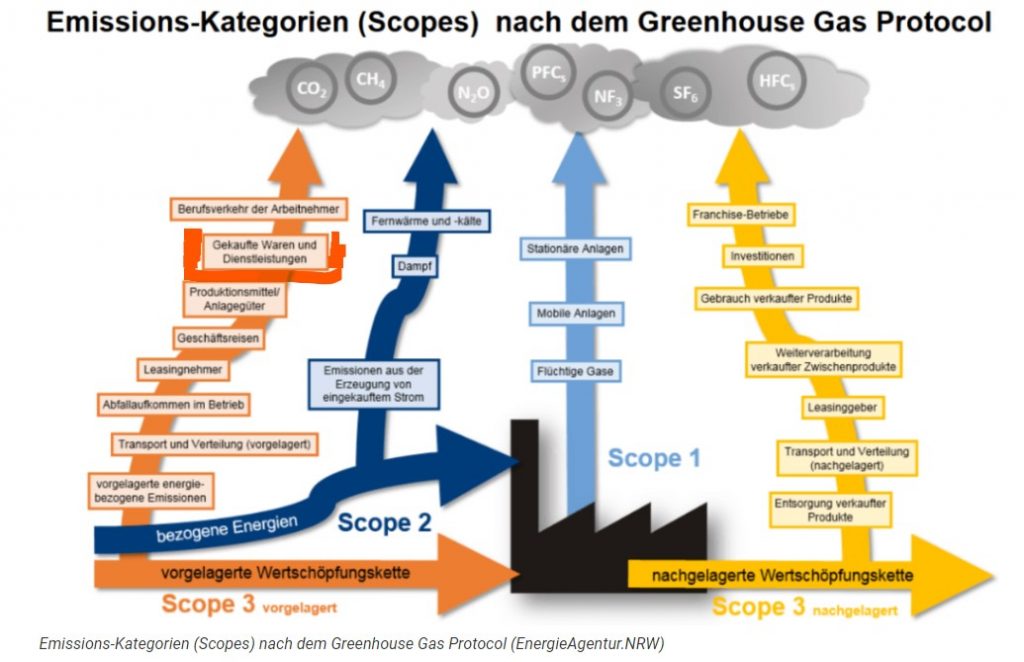

Even if you are not directly affected by the Corporate Sustainability Reporting Directive (= guideline for corporate sustainability reporting), your customers and partners can and will approach you with related questions. See also the carbon footprint graphic. We will help you answer these questions.

Your added value!

You demonstrate to your customers, employees, applicants, and other interested parties that your company assumes social responsibility. You reduce costs in the medium term through sustainable corporate management. You strengthen customer and employee loyalty. You comply with legal requirements.

As a company directly or indirectly affected by the CSRD, you can integrate sustainability requirements into your existing management system.

- In a quality management system according to ISO 9001, this can be done partly through the requirements of interested parties (ISO 9001 Chapter 4.2).

- In an environmental management system according to ISO 14001 or EMAS III, this can be done partly through the binding obligations (ISO 14001 Chapter 6.1.3), the environmental aspects/life cycle assessment (ISO 14001 Chapter 6.1.2), and the requirements of interested parties (ISO 14001 Chapter 4.2).

- In the energy management system according to ISO 50001, this can be partially achieved through the requirements of interested parties (ISO 9001 Chapter 4.2).

- In the social responsibility management system according to ISO 26000 et seq., this can be achieved entirely.